When the social media platform Snapchat was blowing up, it launched a feature called Snapcash. This tool allowed users to transfer money to each other using Snapchat cash transfers. The tool was discontinued in 2018 for numerous reasons, but there are some lessons for marketers to learn from this innovative feature and how it influenced today’s social payment apps.

In this blog, we’ll explore what Snapcash was, how it enabled users to share money on Snapchat, and some key takeaways to keep in mind after its discontinuation.

What Was Snapcash?

Can you send money on Snapchat? Well, you once could.

Snapcash was a peer-to-peer payment system native to Snapchat. Users could easily request or send money through Snapchat right in chat, preventing users from leaving the app to complete transactions.

The app came along in 2014 through a partnership with Square, a provider of payment systems for businesses.

Why Snapcash Was Discontinued

In 2018, Snapchat and Square’s partnership dissolved, and this feature was discontinued. While a particular reason was never given by either company for dropping the feature, experts have speculated that it likely resulted from multiple factors, such as:

- Stiff competition against other payment apps, including PayPal and Venmo

- Privacy and security concerns around transactions and financial data

- Limited adoption among its users, likely due to said competition

You might ask: Can you send money through Snapchat in any other way? At this time, users on the platform will need to use a third-party payment app to complete transactions, such as PayPal or Zelle.

How Snapcash Worked

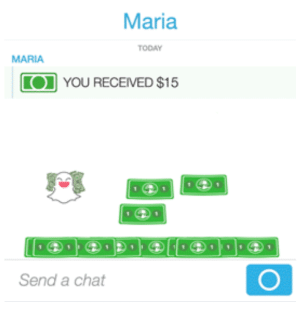

So, how can you send money through Snapchat using this tool? Here was how it worked:

- Users would log into the Snapchat app.

- In their account settings, users would then choose “Snapcash” and add a debit card. The app only accepted Mastercard or Visa debit cards, which could have contributed to its limited adoption.

- Once set up, users could open a chat with the intended recipient.

- By typing “$” followed by a dollar amount, Snapchat recognized an attempted transaction, prompting the green Snapcash button to appear.

- Users could tap the button to transfer money through Snapchat.

To receive money on Snapchat, recipients would need to have a Snapchat account with a linked debit card, through which the money would transfer to the person’s bank.

Legacy Impact: What Marketers Can Learn

Marketers can take away certain lessons from Snapcash’s rise and fall, including:

1. The Value of New Feature Integration

One of the key elements that made Snapcash a temporary success was its integration of fintech with social media, as users no longer wondered how to send money on Snapchat with this convenient feature.

This particular type of integration may not be the solution in your case, but it highlights how making things convenient for your audience can maximize engagement.

2. The Importance of Trust and Security

One key potential reason Snapcash shut down could have been due to concerns regarding user privacy and security, which eventually corroded users’ trust in the feature.

Whenever launching a new feature or platform, it’s essential to ensure users’ privacy and keep data secure, complete with an accessible privacy policy. Taking the right measures can go a long way in building and maintaining your audience’s trust.

3. The Need for User Adoption at Scale

Snapchat faced a lot of competition when launching Snapcash, with so many other convenient social payment apps available. While many users engaged with Snapchat’s feature, there wasn’t enough overall adoption to make it sustainable.

Whenever rolling out a feature, product, or service, marketers need to do what they can to differentiate their offering from competitors, incorporating and highlighting advantages that they won’t find elsewhere.

Social Payment Apps in 2025

Let’s look at the various social payment apps and some of the social features they offer compared to Snapcash:

| Feature | Snapcash | Venmo | Cash App | Zelle | Apple Cash | Google Pay | PayPal |

| Social Feed | No feed, purely private | Includes a private and public feed to display transactions | No feed | No feed | No feed | No feed | Limited public feed similar to Venmo |

| User Profile | Displayed Snapchat name | Allows users to create a unique Venmo profile | Users can create $Cashtag usernames | Profile is purely tied to the user’s bank account contact details | Transactions tied to Apple ID | Uses Google Account profile | Distinct profile with a custom PayPal.Me link |

| Emojis / Notes | Users could use text and emojis in payment messages | Enables users to implement emojis and notes with each transaction | Notes are optional, but not in a social context | No emojis or text permitted | Allows users to add a memo when sending through iMessage | Gives users the ability to add notes | Private notes allowed |

| Platform Integration | Seamlessly integrated into Snapchat messaging | PayPal runs this service with third-party integration into other apps and PayPal services | Works within Square’s ecosystem, along with other financial services | Compatible across hundreds of American banking apps | Integrated into the entire Apple ecosystem, including Apple Wallet, Messages, and Siri | Like Apple, deeply integrated into Google’s ecosystem, including Google Wallet and Android devices | A much broader scope with integrations for millions of platforms |

| Social Focus | Not designed for social interaction | Encourages social sharing to engage users | Focused primarily on efficient and private transactions | Entirely focused on security, privacy, and efficiency | Connects to messaging, but there is no dedicated social feed | Focused on private transactions | Incorporates PayPal.Me and messaging, but no focus on social |

Social Commerce and Messaging Payments Today

With Snapchat cash transactions nonexistent, there are still plenty of social media platforms out there that allow you to complete in-app transfers.

Here are some of them and their integrations:

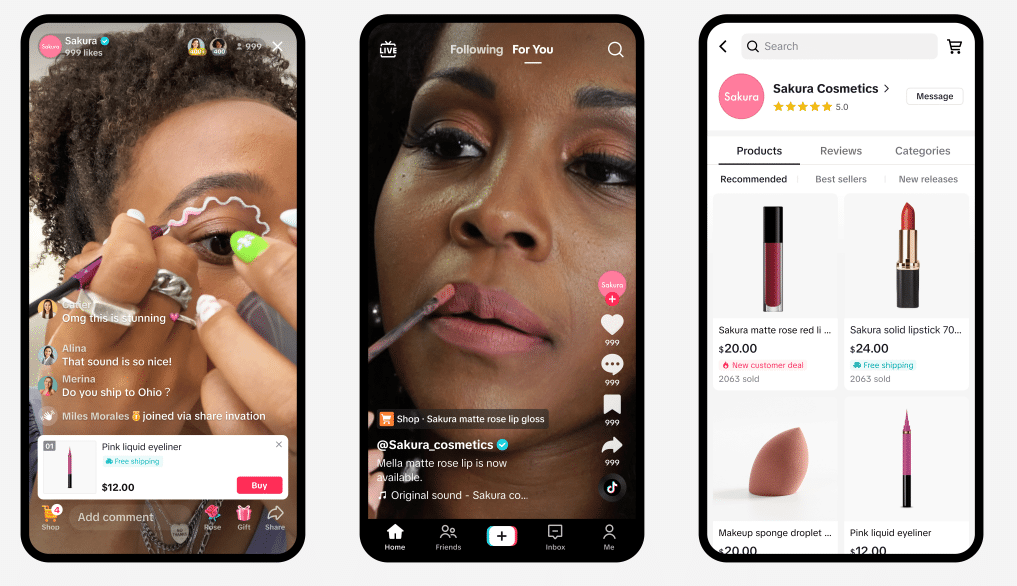

TikTok

One social media app with fintech integration is TikTok, which features an entire economic ecosystem fueled mostly by TikTok Shop, an ecommerce feature allowing people to make purchases right from the app.

The app features multiple third-party integration via TikTok Shop, allowing users to complete transactions using PayPal, Stripe, Apple Pay, and Google Pay, among other methods.

However, TikTok Shop has struggled to find a footing in North America because of the many competitors and various user behaviors.

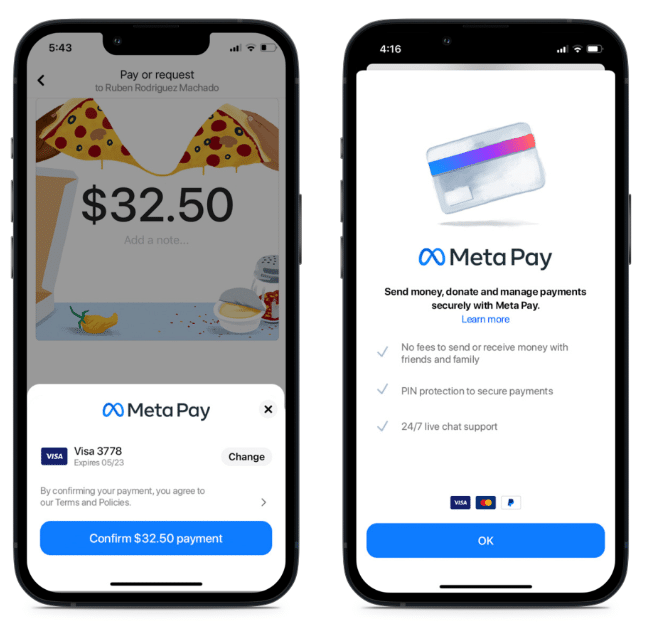

Another platform with a financial component is Instagram, which operates using Meta Pay and allows users to securely store their debit and credit card information.

Using the Messenger API in Instagram, users can easily pay businesses and users directly with the “Pay” button in chat.

What began as a basic messaging app has since grown into a seamless commerce tool, particularly in regions like India, Singapore, and Brazil. Integrations include India’s Unified Payments Interface (UPI) and, in Brazil, Meta Pay.

Businesses can also use the WhatsApp Business API to request payments through chat, enabling customers to choose their preferred payment method.

One of China’s most popular payment apps, WeChat, through WeChat Pay, makes it easy for users to perform a range of financial tasks, from paying bills to buying from businesses.

Merchants can create a QR code that customers scan to complete payments. This system is integrated in public services, food delivery, and transportation, among other areas, creating a cohesive ecosystem.

Future of Social Payments

Whether transferring money to family or friends or making a purchase from a business, there are some innovations that will continue to make social payments more secure and convenient.

Some predictions for the future include:

- AI-Driven Fraud Detection: Algorithms in social apps will be able to use AI and machine learning to identify fraudulent users and transactions, typically by analyzing user behavior like typing speeds and certain patterns.

- Cross-Border Peer-to-Peer: AI and blockchain will also contribute to international transactions using social platforms, offering frictionless yet secure payment while bypassing conventional banking intermediaries.

- Embedded Wallets in Social Apps: More social apps will continue to include their own wallets, engaging users more effectively and keeping them on the app to conveniently complete transactions and transfers.

FAQs

1. What was Snapcash?

Snapcash was a peer-to-peer payment service on Snapchat that the platform introduced in 2014, enabling users to send money through Snapchat directly to other users. The service came from a partnership with Square until Snapchat discontinued it in 2018.

2. Why did Snapcash shut down?

Although successful during its run, Snapcash shut down in 2018 for a combination of reasons, including its competition with other social payment apps like Venmo and PayPal, security and privacy concerns, and an overall shift in strategy. However, Snapchat has not officially disclosed the specific reasons.

3. Does Snapchat still let you send money?

You might ask, “Can you send money on Snapchat?” While Snapcash is no longer a feature, leaving users no way to send money through Snapchat directly, you can still send money to Snapchat users with third-party social payment apps, including Venmo, PayPal, and Cash App.

4. What replaced Snapcash?

You might wonder how to send money on Snapchat with Snapcash gone. While users cannot transfer money through Snapchat right on the platform, they can still go through other third-party apps, such as Cash App, PayPal, Venmo, Zelle, and Facebook Meta Pay.

5. What can marketers learn from Snapcash?

There are multiple lessons that marketers can learn from this feature, from its introduction to its end. For example, marketers can see the value of integrating social media with fintech, the equal values of trust and security, and the need to encourage large-scale user adoption.

Get the Most From Social Marketing With Ignite Visibility

Snapcash may be gone, but its ephemeral existence taught marketers the risks and rewards of integrating a new feature to appeal to customers. If you want to develop a successful social media marketing strategy or a comprehensive digital marketing solution, Ignite Visibility can help with this through a fully tailored campaign.

When you work with us, you’ll be able to:

- Pinpoint the best platforms to use

- Connect with the right target audiences

- Establish convenient payment methods for customers via social payment apps and other channels

- Continually optimize your strategy with real-time reporting and analytics

- And more!

Get in touch with us today to request a free proposal and find out what Ignite can do for your business.